Peak Inflation?

…Have we seen peak inflation?…probably:

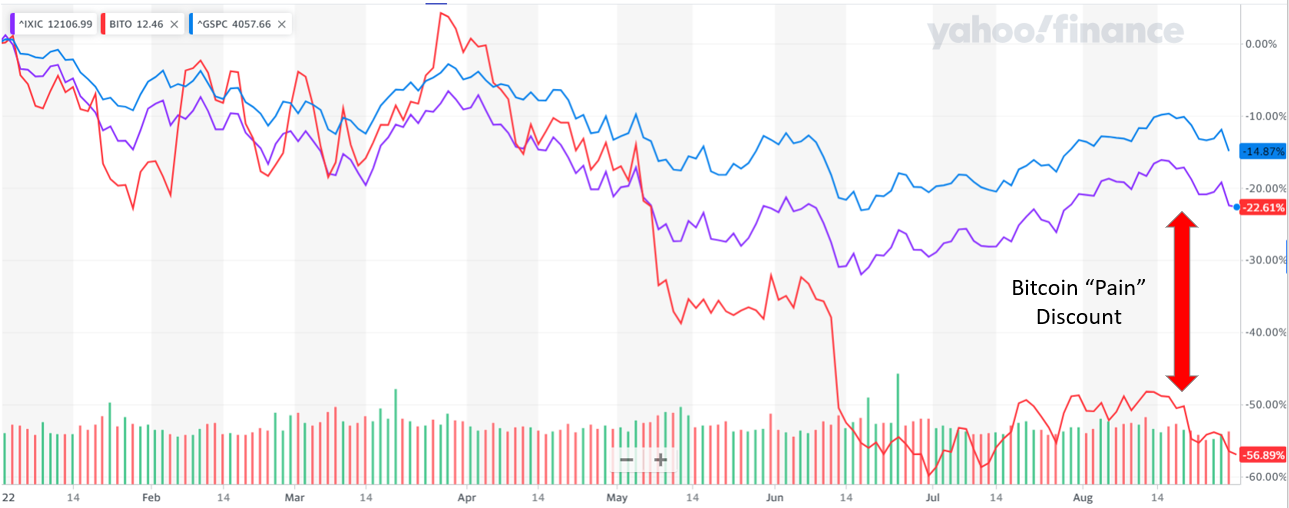

However, the market also probably over-reacted to the upside (or more likely, this catalyzed a short-covering rally). Either way, US Federal Reserve governor Christopher Waller was quick to say “Everybody should just take a deep breath and calm down, We’ve got a ways to go.” He also suggested a “higher for longer” type scenario which could change investors’ calculus on a “pivot” next year.

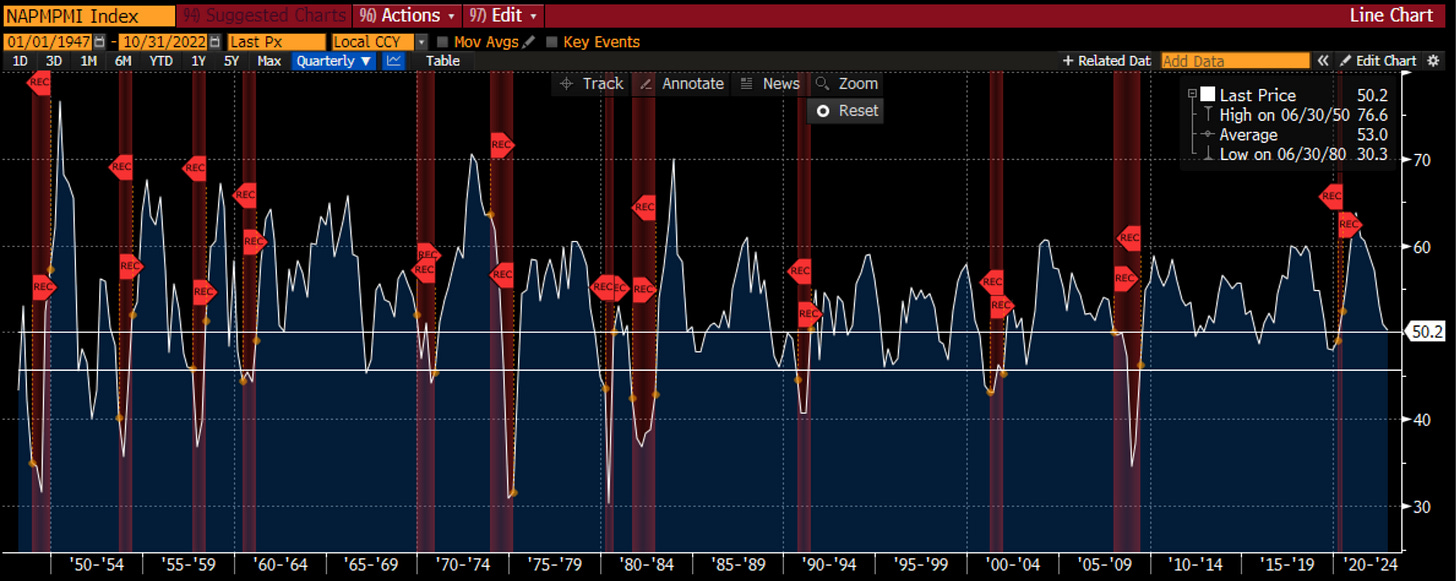

While there are several dozen interesting macro datapoints to consider, one of the most useful ones for establishing general risk appetite is the ISM. Richard Excell at the Gies College of Business at the U of Illinois (You can sign up for his newsletter here) has some great insights here. He shows the following ISM chart and notes:

“that the only period with negative average returns for stocks over time is when the ISM is below 50 and falling. Investors know this and thus try to be out of stocks when this happens. If the ISM is below 50 but rising, this is often the best period for equity returns because this is when the economy is in recovery. Above 50 and falling is also positive returns and this is why near inflections, we can see such choppy price action.”

“Interestingly, a recession doesn’t correspond with 50 in the ISM. This is even though 50 is the % of respondents that say things are getting better vs. worse. However, historically, a recession doesn’t happen until ISM drops below 47 actually. I have drawn those lines on the chart. You can see several dips below 50 in the post GFC era when a recession didn’t happen. You can also see this in the 90s and in the 60s. You have seen many, and I have shown several, different overlays of these various periods to see if any resemble the current. JayPo wants us to think it is the 90s and a soft-landing. Many others point to the 60s & 70s. Regardless, we are on the brink of dropping below 50 which is bad for stocks, but will we go into a recession?”

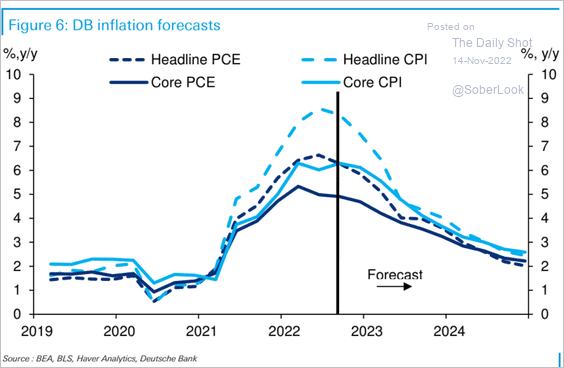

“New Normal” Inflation Rate?

While we might have some clarity on the fact that inflation is finally headed lower…an important question (that we’ve been asking for months) is how low can it go?

Interestingly, more Wall St. banks are now coming out and calling that the Fed will be forced to increase their target inflation rate as early as next year (which has been our view for several months). A good rationale, is that in order to bring inflation back down (all the way) to 2% sustainably, would require a very large unemployment rate for some time (e.g. 6+%). For those looking for a deep-dive on this, Jason Furman (of Harvard) lays this out very well in a series of tweets from September:

Under these scenarios if the unemployment rate rises to 4.1% then inflation will stay above 3%. If it rises to 7.5% then inflation will slightly undershot the Fed's target.

The unemployment rate needed to hit the Fed's target in this scenario is 6.4%. pic.twitter.com/ysUDUU6yaG

— Jason Furman (@jasonfurman) September 8, 2022

The bottom line is, getting inflation back down to 2% on a sustained basis is a bigger lift than many investors appreciate and comes at the very real cost of high unemployment…

The alternative is to allow a little bit of inflation creep (“style drift” would be the appropriate analogy for investors), which has the dual benefit of:

(i) mitigating some of the unemployment pain and

(ii) effectively “monetizing” some of the massive debtload (remember Weimar Germany post Marshal plan?)

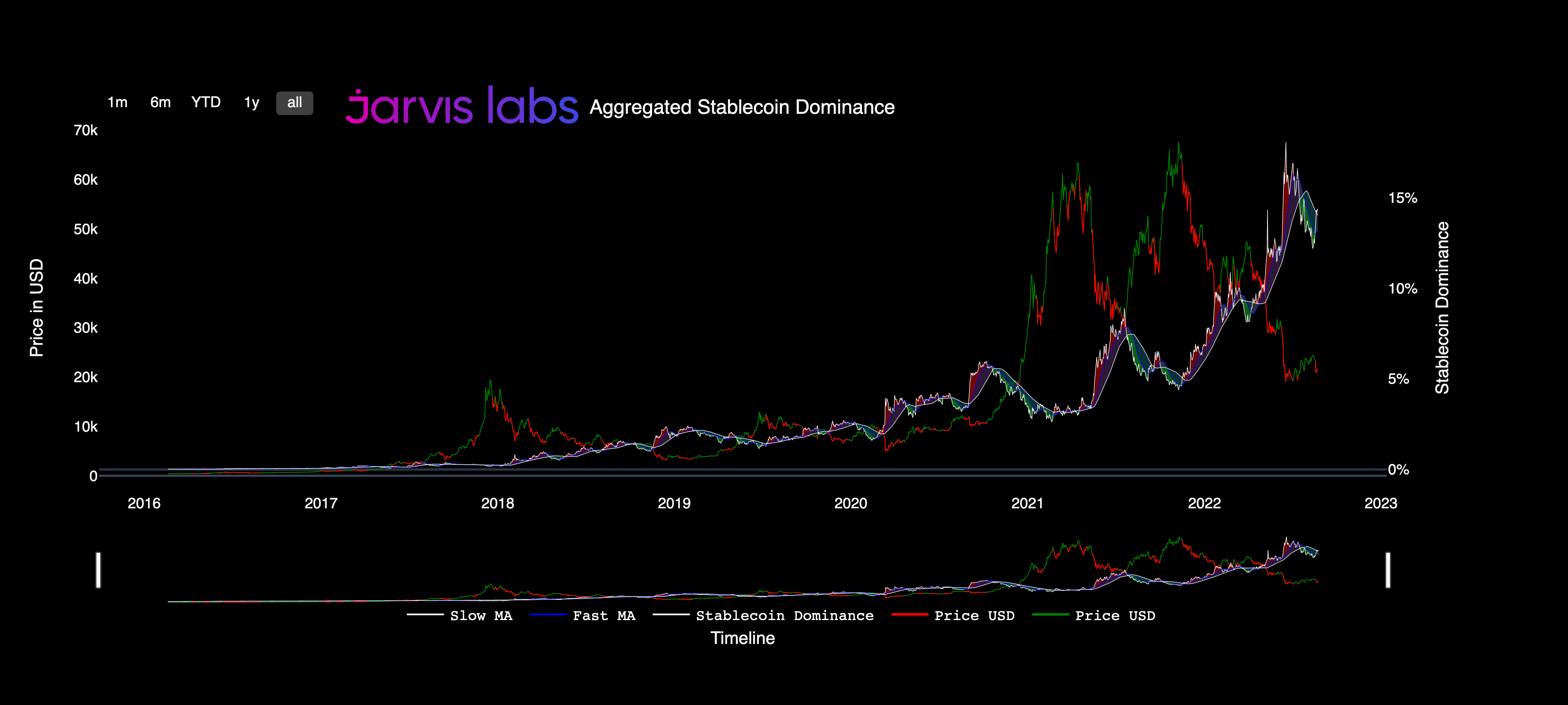

The key takeaway of this is that it sets up a potentially very good secular tailwind for commodities and hard assets over the next decade. For those that thought the commodities “trade” might be over, normalizing a higher inflation rate could end up being a powerful force which will manifest in higher hard assets prices for years to come.

For those who are looking to learn more about Bitcoin, specifically how to talk to clients about the digital asset and it’s potential value in asset allocation models, we put together a high-level guide called “The Fiduciary’s Guide to Bitcoin and Blockchain”. Click on the button to the right to head to access the guide.

https://idxdigitalassets.com/wp-content/uploads/2022/11/FTX-whats-next.png

292

858

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2022-11-14 13:47:202022-11-15 09:49:52FTX Blowup and What it means for Crypto?

https://idxdigitalassets.com/wp-content/uploads/2022/11/FTX-whats-next.png

292

858

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2022-11-14 13:47:202022-11-15 09:49:52FTX Blowup and What it means for Crypto? https://idxdigitalassets.com/wp-content/uploads/2022/11/peak-inflation.png

291

822

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2022-11-14 12:15:372022-11-14 12:16:11Peak Inflation & Inflation Targets

https://idxdigitalassets.com/wp-content/uploads/2022/11/peak-inflation.png

291

822

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2022-11-14 12:15:372022-11-14 12:16:11Peak Inflation & Inflation Targets https://idxdigitalassets.com/wp-content/uploads/2022/08/thoughts_CIO_pivot_pain.png

324

906

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2022-08-29 09:20:522022-09-06 18:38:26Pivot, Pain & Powell….What Does This Mean for Crypto?

https://idxdigitalassets.com/wp-content/uploads/2022/08/thoughts_CIO_pivot_pain.png

324

906

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2022-08-29 09:20:522022-09-06 18:38:26Pivot, Pain & Powell….What Does This Mean for Crypto? https://idxdigitalassets.com/wp-content/uploads/2022/06/where-do-we-go.png

243

519

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2022-06-07 09:19:362022-06-10 07:30:24Bitcoin…where to go from here?

https://idxdigitalassets.com/wp-content/uploads/2022/06/where-do-we-go.png

243

519

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2022-06-07 09:19:362022-06-10 07:30:24Bitcoin…where to go from here? https://idxdigitalassets.com/wp-content/uploads/2021/10/thoughtsCIOBTCATH-1.png

405

720

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2021-10-20 09:45:432021-10-20 15:57:06Bitcoin Hits an All-Time-High

https://idxdigitalassets.com/wp-content/uploads/2021/10/thoughtsCIOBTCATH-1.png

405

720

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2021-10-20 09:45:432021-10-20 15:57:06Bitcoin Hits an All-Time-High https://idxdigitalassets.com/wp-content/uploads/2021/10/Bitcoinetfblog.jpg

405

720

Drew Acocella

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Drew Acocella2021-10-18 14:19:142021-10-18 14:19:14Bitcoin ETFs: What Investors Need to Know About This Structure

https://idxdigitalassets.com/wp-content/uploads/2021/10/Bitcoinetfblog.jpg

405

720

Drew Acocella

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Drew Acocella2021-10-18 14:19:142021-10-18 14:19:14Bitcoin ETFs: What Investors Need to Know About This Structure https://idxdigitalassets.com/wp-content/uploads/2021/05/cryptolendingblog.png

575

995

Drew Acocella

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Drew Acocella2021-08-05 15:17:522021-09-07 12:53:27Understanding the 3 Primary Risks in Digital Assets Lending

https://idxdigitalassets.com/wp-content/uploads/2021/05/cryptolendingblog.png

575

995

Drew Acocella

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Drew Acocella2021-08-05 15:17:522021-09-07 12:53:27Understanding the 3 Primary Risks in Digital Assets Lending https://idxdigitalassets.com/wp-content/uploads/2021/05/eip1559.png

600

1200

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2021-07-20 10:00:312021-09-07 17:04:59Ethereum 2.0 & EIP-1559: What it All Means for ETH

https://idxdigitalassets.com/wp-content/uploads/2021/05/eip1559.png

600

1200

Ben

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Ben2021-07-20 10:00:312021-09-07 17:04:59Ethereum 2.0 & EIP-1559: What it All Means for ETH https://idxdigitalassets.com/wp-content/uploads/2021/06/cryptobankingblog.jpeg

636

1000

Drew Acocella

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Drew Acocella2021-06-07 22:01:532021-09-07 12:54:42Crypto Banking 101

https://idxdigitalassets.com/wp-content/uploads/2021/06/cryptobankingblog.jpeg

636

1000

Drew Acocella

https://idxdigitalassets.com/wp-content/uploads/2022/08/imageedit_1_3451532283.png

Drew Acocella2021-06-07 22:01:532021-09-07 12:54:42Crypto Banking 101